Archive

CRA’s Transition to Online Mailing Platform as Default

Leave a CommentTHE COMMUNICATION BELOW APPLIES TO CORPORATIONS AND SELF-EMPLOYED INDIVIDUALS

Starting May 12, 2025, the Canada Revenue Agency (CRA) will transition to online mail as the default method for delivering most business correspondence. This change is part of the CRA’s ongoing efforts to improve service delivery. As a result, most notices and other communications will be delivered through the CRA’s secure online portal instead of by paper mail.

To ensure you don’t miss important communications from the CRA, we strongly recommend logging into or registering for My Business Account and ensuring your contact information is up to date. By adding an email, you’ll receive notifications when there are updates to your account or when new mail is available in My Business Account, prompting you to log on and check your online mail. Up to three email addresses can be added to each program account, and you can also add authorized individuals. Please note – do not use any Ritchie Shortt & Tully LLP email addresses as a contact for CRA correspondence, as we are not responsible for managing any emails from the CRA on your behalf.

To prepare for the change to online mail, the CRA recommends signing in to your CRA account to ensure you have access to all your business numbers and the ability to view your business correspondence. If you are not registered and would like to take advantage of the benefits of a CRA account, go to Register for a CRA account.

The default for correspondence will be online mail, whether you have an email address on file or not. This is why there may be action required on your part. We strongly recommend you get set up with a CRA account for your business and/or log on to your CRA account and check/add an email address to your business profile.

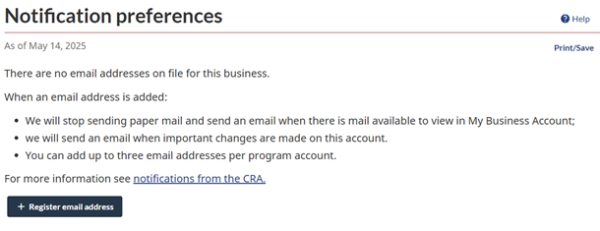

There are 2 sections to check once you are logged on to your account:

1. On the left side bar, “Profile”, “Notification preferences” – this is where you can add or edit your email address.

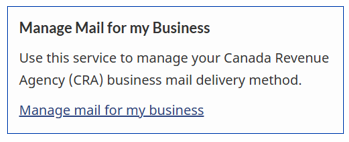

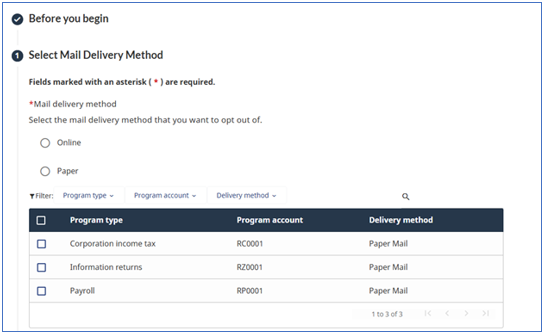

2. On the left side bar, “Profile”, “Manage mail for my business” – This is where you can select your preference. Here you will need to select what method you are opting out of. Therefore, select “Paper” to enrol for online (or select “Online” to receive paper mail).

2. On the left side bar, “Profile”, “Manage mail for my business” – This is where you can select your preference. Here you will need to select what method you are opting out of. Therefore, select “Paper” to enrol for online (or select “Online” to receive paper mail).

For more details, you can visit canada.ca/cra-business-mail-online and here Email notifications from the CRA – Businesses – Canada.ca.

If you prefer to continue receiving paper mail, you will need to either submit a request via Form RC681 – Request to Activate Paper Mail for Business which needs to be mailed to the CRA or via your My Business Account profile as outlined above starting May 12, 2025. Please click here for a copy of the form.

To keep receiving paper mail you will need to make a request to activate paper mail every two years and you will be responsible for such submission to ensure you continue receiving paper mail. The effective date of this change for existing businesses is June 16, 2025. Therefore, if you would like to request the paper mail option for business you should act quickly on this as there is a potential postal strike.

If you require assistance, please reach out to general@rstaccountants.com.

Government of Canada: Deferral of change in capital gains inclusion rate

Leave a CommentOn January 31, 2025, it was announced that the federal government is deferring—from June 25, 2024 to January 1, 2026—the date on which the capital gains inclusion rate would increase from one-half to two-thirds on capital gains realized annually above $250,000 by individuals and on all capital gains realized by corporations and most types of trusts.

(In the 2024 Federal Budget, the Federal Government proposed that the inclusion rate for capital gains for corporations, individuals and trusts would increase from one-half to two-thirds of the actual capital gain and that individuals would retain the one-half inclusion rate on the first $250,000 of capital gains annually. The increase was proposed to be effective for capital gains realized on or after June 25, 2024. The capital gains inclusion rate represents the portion of capital gains that is taxable.)

Under the original proposal, the government had proposed to increase the Lifetime Capital Gains Exemption to $1.25 million, effective June 25, 2024, on the sale of certain small business shares and farming and fishing property. This proposal remains in place.

In Budget 2024, the government had also announced a new Canadian Entrepreneur’s Incentive beginning in the 2025 tax year. The inclusion rate will be one-third on up to $400,000 of eligible capital gains. After 2025, the maximum would increase by $400,000 each year, reaching $2 million in 2029. This proposal remains in place.

This all remains as proposed legislation and not law until a new bill is introduced. However, it provides clarity that the 2024 tax returns can be filed at the one-half inclusion rate.

If your corporate or estate tax return has already been filed using the proposed two-thirds capital gains inclusion rate, we will follow up with you on next steps.

Please see the linked Commentary for more details on these items.

IMPORTANT UPDATE – Bare Trust Reporting Exemption

Leave a CommentOn March 28, 2024 the CRA announced that bare trusts would be exempt from trust reporting requirements for 2023. CRA stated:

“To support ongoing efforts to ensure the effectiveness and integrity of Canada’s tax system, the Government of Canada introduced new reporting requirements for trusts.

In recognition that the new reporting requirements for bare trusts have had an unintended impact on Canadians, the Canada Revenue Agency (CRA) will not require bare trusts to file a T3 Income Tax and Information Return (T3 return), including Schedule 15 (Beneficial Ownership Information of a Trust), for the 2023 tax year, unless the CRA makes a direct request for these filings.

Over the coming months, the CRA will work with the Department of Finance to further clarify its guidance on this filing requirement. The CRA will communicate with Canadians as further information becomes available.”

For more information, see CRA’s Read more

New and Expanded Trust Reporting

Leave a CommentNew and Expanded Trust Reporting: It’s Here!

New rules aimed at providing more transparency on beneficial ownership of assets now require that more trusts (and estates) file tax returns. These changes will catch many individuals and businesses that may not be aware of their trust-like relationships, exposing them to potential penalties and other consequences for non-compliance. The rules become effective in 2023, with a filing deadline of April 2, 2024.

Unexpected exposure – bare trust arrangements

The rules have been expanded to include cases where a trust acts as an agent for its beneficiaries, commonly known as a bare trust. In such instances, the person/entity listed as the owner of an asset is not the true beneficial owner; instead, they hold the asset on behalf of another party.

STEP 1: Does a bare trust arrangement exist?

To determine if a bare trust arrangement exists, the following question should be asked:

- Is the person on title or holding the asset the true beneficial owner? For example, do they get the benefits of the asset (such as sale proceeds) and bear the costs or risks of the asset (such as property taxes)?

There is likely a bare trust arrangement if there is a mismatch between legal and beneficial ownership, often requiring a trust return.

There are several reasons why an individual, business or organization may use a bare trust arrangement. Many parties involved in a bare trust arrangement may not realize that they are, much less that there may be a filing requirement with CRA. No lawyer may have ever been involved, and no written agreement may have ever been drafted.

While there are countless possibilities of bare trust arrangements, the following lists some common potential examples.

Individual Reasons

- a parent is on title of a child’s home (without the parent having beneficial ownership) to assist the child in obtaining a mortgage;

- a parent or grandparent holds an investment or bank account in trust for a child or grandchild;

- one spouse is on title of a house or asset although the other spouse is at least a partial beneficial owner;

Estate Planning Reasons

- a child is on title of a parent’s home (without the child having beneficial ownership) for probate or estate planning purposes only;

- a child is on parent’s financial accounts (or other assets) to assist with administration after the parent’s passing;

Business Administration Reasons

- a corporate bank account is opened by the shareholders with the corporation being the beneficial owner of the funds;

- a corporation is on title of an individual’s real estate, vehicle or other asset, and vice-versa;

- assets registered to one corporation but beneficially owned by a related corporation;

- use of a nominee corporation for real estate development purposes;

- a partner of a partnership holding a bank account or asset for the benefit of all the other partners of a partnership;

- a joint venture arrangement where the operator holds legal title to development property as an agent for the benefit of other participants;

- a cost-sharing arrangement where a person holds a business bank account, or other assets, to facilitate the arrangement while having no, or only partial, beneficial interest in these shared assets;

Industry-specific Issues

- a property management company holding operational bank accounts in trust for their clients, or individuals managing properties for other corporations holding bank accounts for those other corporations; and

- a lawyer’s specific trust account (while a lawyer’s general trust account is largely carved out of the filing requirements, a specific trust account is not).

CRA has not commented on several of the examples; it is uncertain how they will interpret and enforce the law.

STEP 2: Does a trust return need to be filed?

After determining that a bare trust arrangement exists, it is important to determine whether an exception from filing a trust return is available.

Some of the more common exceptions include the following:

- trusts in existence for less than three months at the end of the year;

- trusts holding only assets within a prescribed listing that is very restrictive (such items in the listing include cash and publicly listed shares) with a total fair market value that does not exceed $50,000 at any time in the year;

- trusts required by law or under rules of professional conduct to hold funds related to the activity regulated thereunder, excluding any trust that is maintained as a separate trust for a particular client (this applies to a lawyer’s general trust account, but not specific client accounts); and

- registered charities and non-profit clubs, societies or associations.

A trust return must be filed if one of the exceptions are not met. Even where one of the new exceptions is met, a trust would still have to file a return if they had to file under the prior rules, such as the trust having taxes payable or having disposed of capital property.

STEP 3: What information must be disclosed?

Where a trust is required to file a tax return, the identity of all the trustees (who is on title or holds the asset), beneficiaries (who really owns the asset), settlors (who owned the asset originally) and anyone with the ability to exert influence over trustee decisions regarding the income or capital of the trust must be disclosed.

Such required information includes:

- name;

- address;

- date of birth (if applicable);

- country of residence; and

- tax identification number (e.g. social insurance number, business number, trust number).

Obtaining this information proactively is especially helpful, particularly if those involved are no longer in close contact.

Traditional trusts

Under the previous rules, a trust was required to file a trust return if one of several conditions were met, such as the trust having taxes payable or disposing of capital property. Many trusts did not meet a condition and, therefore, were not required to file a trust return previously. For example, many trusts owning shares of a private corporation were historically not required to file in years when there were no share sales or dividends received. However, trusts that were exempted from filing under the old rules are now required to file unless one of a new set of narrow exceptions is also met. See some of the more common exceptions in STEP 2 above.

Under the new rules, some of the more common trusts that may require disclosure include the following: trust owning shares of a private corporation, trust owning a family cottage, spousal or common-law partner trust, alter-ego trust and testamentary trust.

Failing to File… So what?

Failure to make the required filings and disclosures on time attracts penalties of $25/day, to a maximum of $2,500, as well as further penalties on any unpaid taxes. New gross negligence penalties may also apply, being the greater of $2,500 and 5% of the highest total fair market value of the trust’s property at any time in the year. These will apply to any person or partnership subject to the new regime.

CRA has recently indicated that, for bare trusts only, the late filing penalty would be waived for the 2023 tax year in situations where the filing is made after the due date of April 2, 2024. However, CRA noted that this does not extend to the penalty applicable where the failure to file is made knowingly or due to gross negligence. As there is limited guidance as to who would qualify, it is recommended that disclosures should be made in a timely manner.

In addition to penalties, failing to properly file trust returns may result in negative tax (such as possibly losing access to the principal residence exemption) and non-tax (such as inadvertently exposing assets to creditors inappropriately) consequences.

This information is for educational purposes only. As it is impossible to include all situations, circumstances and exceptions in a summary such as this, a further review should be done by a qualified professional. No individual or organization involved in either the preparation or distribution of this document accepts any contractual, tortuous, or any other form of liability for its contents or for any consequences arising from its use.Copyrighted ©Video Tax News Inc. 2024. Distributed with permission. Date of Issue – January 2024 |

|

If you have any questions, give us a call! |

Enhanced Trust Reporting Requirements in Effect

Leave a CommentAs part of the 2018 Federal Budget, enhanced reporting for trusts was announced in an effort to increase transparency and help authorities combat the misuse of corporate vehicles to lower income taxes. The 2019 Federal Budget confirmed the Federal Government’s intention to proceed with introducing the enhanced reporting requirements. The enhanced reporting requirements were initially expected to be applied for the 2021 taxation year. However, the implementation was deferred until Bill C-32 (Fall Economic Statement Implementation Act, 2022) came into force.

Beginning in the 2023 taxation year, many trusts which were not previously required to file an annual income tax (T3) return will be required to do so. The deadline to file a return is 90 days after the trust’s tax year-end, generally March 31st for trusts with a December 31st tax year-end(except on leap years where the deadline will be March 30th).

Trusts will also be required to provide additional information detailing the trustees, beneficiaries, settlors, and any person who has the ability to influence or override a decision of the trustee(s), such as a protector. The information will be contained on a beneficial ownership schedule and is filed together with the T3 return; it cannot be filed separately.

The penalties for late filing the T3 return and beneficial ownership schedule will be $25 per day ranging from $100 to $2,500. For instances of gross negligence, or knowingly failing to file the information, an additional penalty equal to 5% of the maximum value of the property held during the relevant year will apply and will not be less than $2,500. These penalties are in addition to the existing failure to file penalties and interest for late payments.

For bare trusts, CRA is providing proactive relief by waiving the late filing penalty for the 2023 tax year in situations where the T3 return and beneficial ownership schedule are filed after the deadline. However, the gross negligence penalty has not been waived and may be levied by CRA in instances of gross negligence or knowingly failing to file the information.

Bare trusts can exist in both formal and informal arrangements. Two common examples of informal bare trusts are: (1) when a parent is on title to a property owned by their child for financing purposes only and does not have a beneficial interest in the property, and (2) when a child is on title to a property owned by their parent for probate planning purposes. In both instances, a bare trust exists and would be subject to these additional reporting requirements. There has not yet been any relief offered in respect of these informal trusts and filing would be required.

There are some exemptions to the enhanced reporting requirements which allow a trust not to provide the additional information and not file a T3 return. These exemptions include trusts that are graduated rate estates, qualified disability trusts, trusts that have been in existence less than 3 months, trusts which hold less than $50,000 in assets throughout the taxation year if the holdings are limited to deposits, government debt obligations, and listed securities, and other non-express trusts. An analysis must be completed to determine whether a trust could be exempt from filing under these new enhanced reporting rules.

If you would like our assistance in determining whether these enhanced reporting requirements apply to your trust, be sure to contact us for further information.

The Underused Housing Tax (UHT) Act

Leave a CommentIn June 2022, the Underused Housing Tax (UHT) Act received royal assent and became law. The act imposes a 1% tax on the value of residential properties that are vacant or underused which are owned by entities other than permanent residents or Canadian citizens.

The legislation is retroactive to January 1, 2022 and returns will follow a calendar year reporting period. A return in respect of the UHT will be due April 30 each year, even if no UHT is owed. The first return will be due May 1, 2023 (since April 30 is a Sunday). A late filing penalty of up to $10,000 may be charged on returns filed after the due date, and an additional penalty will be charged on the UHT due that was not paid.

The UHT covers detached homes with up to three units (i.e., single family home, duplex, triplex), semi-detached homes, row houses, and condominiums.

Properties excluded from the UHT include residential properties that are uninhabitable for at least 120 days in the year due to renovations, residential properties if the owner died during the current or previous calendar year, and vacation properties located in rural areas and used personally by the owner, owner’s spouse or common-law partner for at least four weeks in the calendar year.

The Act applies to housing owned directly or indirectly, in whole or in part, by non-residents or non-Canadians. The residency test for this Act is not the same as the income tax concept of residency.

Excluded owners who are not required to file a UHT return include Canadian citizens and permanent residents, registered charities, and co-operative housing corporations, among other entities.

Private companies, partnerships, and trusts are not excluded owners and are not excluded from filing a UHT return if they own a residential property. Therefore, it is important that these entities file a return each year, even if there is no UHT owing.

There are various exemptions that may be claimed to eliminate the tax otherwise payable under the Act. Perhaps, most commonly, a private corporation can claim an exemption as a specified Canadian corporation if it is owned less than 10% by foreign individuals or foreign corporations. Partners of partnership and trustees of trusts could also be exempt if they hold an interest in residential property through a partnership or trust.

A UHT return must be filed for owners that are not excluded owners even if an exemption can be claimed to eliminate UHT payable. If a return is not filed, or is filed late, a penalty of up to $10,000 may result. In many circumstances, it is likely that most private corporations holding residential real estate will be required to file a return each year.

The UHT on a vacant or underused residential property is 1% of the home’s value, which is the higher of its most recent sale price or its taxable value. An election may also be filed to use the fair market value determined by an appraiser. Owners with a partial ownership interest in a residential property are each responsible for the UHT based on their ownership interest. The Underused Housing Tax Return and Election Form has recently been released.

We encourage you to reach out to us for further information if you own residential real estate. Please be advised that we will not be filing this return unless requested and it is not part of our year-end file preparation.

The Vacant Home Tax (VHT)

Leave a CommentIn an effort to encourage property owners to increase rental supply, governments across the country have explored implementing a Vacant Home Tax (VHT). Most notably, the municipalities of Toronto and Ottawa have taken steps to implement this tax at the municipal level starting in 2022. Hamilton will have the tax in 2023, with tax due in 2024.

Many other local governments have expressed interest in implementing a VHT at the municipal level, including those in the regions of Peel, York, Halton, and Durham. It is therefore important to keep up to date with news from your municipality to ensure you are informed of your obligations.

The VHT is an annual tax that will be levied on vacant properties starting in 2022, with tax payable beginning in 2023. Under this program, all residential property owners are required to declare the status of their property(s) each year, even if they live there and the property is not vacant. Homeowners may delegate the filing of the declaration to a third party.

If a declaration is not made for a property, the property will be deemed vacant by the municipality and subject to the VHT. In addition, fines for not filing a declaration or making false or deceptive statements range from $250 to $10,000 for each instance. It is therefore paramount that a declaration be filed on time with complete and accurate information.

The VHT is calculated as 1% of the assessed value of the property. This means that a vacant property with a value of $1M would attract VHT of $10,000 in a year. As 2022 is the first year the tax applies, the amount would be payable in 2023. The City of Toronto has set the declaration deadline as February 2, 2023 and a payment deadline of May 1, 2023. Property owners will receive a Vacant Homes Tax Notice in March or April 2023.

The declaration includes different types of property status declarations which would be selected at the time of filing depending on your circumstances. For example, the City of Toronto includes declarations such as:

- Occupied as principal residence of homeowner,

- Occupied as principal resident of a permitted occupant,

- Occupied as a tenanted property,

- Vacant with an eligible exemption, and

- Vacant or deemed vacant / determined vacant

Only properties deemed or determined vacant are subject to the VHT according to the information published by the city. In general, properties must be occupied for six months or more throughout the year to avoid being subject to the vacant homes tax.

Properties may be exempt from the VHT in Toronto if:

- The registered owner dies in the year,

- There are repairs or renovations which prevent occupation of the property,

- The principal resident is in a hospital, long term, or supportive care facility for up to six months,

- There is a transfer of legal ownership to an unrelated person,

- The unit is required for occupation for at least six months in the taxation year for employment purposes by its owner who has a principal residence outside the Greater Toronto Area, or

- There is a court order prohibiting occupancy of the property for at least six months.

As the VHT is being rolled out by different municipalities, the rules may differ by municipality. For example, the declaration deadline for the City of Ottawa is March 16, 2023. Ottawa adds the VHT to your final tax bill due in June. It is important to refer to information published by the municipality governing your property for exact details of this tax.

We encourage you to reach out to us if you own residential real estate for further information. Please be advised that we will not be filing this declaration unless requested.

2021 or 2022 Work Space in the Home Expenses

Leave a CommentOn January 18, 2022, CRA published additional commentary with respect to claims for workspace in the home expenses on personal income tax and benefit returns.

The additional commentary includes an explanation of how spouses who both worked from home in 2021 or 2022 each calculate their work space in the home expenses using the detailed method.

Temporary Flat Rate Method

The temporary flat rate method, which was new for 2020 tax returns, has been extended for personal tax returns for the 2021 and 2022 tax years. Eligible individuals can claim a simplified expense of $2 per work day (up to $500) on their 2021 and 2022 tax returns.

Work days include days that you worked full-time or part-time hours from home either due the requirement of your employer or voluntarily if your employer gave the option to work from home due to the pandemic. You must have worked from home more than 50% of the time for at least 4 consecutive weeks during the pandemic to be eligible and you are not claiming any other employment expenses on line 22900.

You do not need to calculate the size of your workspace, keep supporting documents, or obtain a signed Form T2200S or Form T2200, from your employer to use this method.

The temporary flat rate method is not available if claims are being made for other employment expenses, such as vehicle expenses, or if your employer reimbursed all of your home office expenses. If your employer reimbursed some but not all home office expenses, you are still eligible to use this method.

Optional Detailed Method

The optional detailed method for home office expenses allows you to claim expenses you paid for the period you worked from home. Eligibility for the detailed method is similar to the flat rate method with the additional requirements that you obtain a completed signed Form T2200S, or Form T2200, from your employer and the expenses claimed are used directly in your work during the period.

The CRA has also published a list of home office expenses for employees and guidance on how to determine your work space use.

If you are expecting to make a claim on your 2021 or 2022 personal tax return using the detailed method, you should reach out to your employer to ensure you get a signed T2200S. In addition, all supporting invoices should be kept to support the claim under the detailed method. To make a claim on your 2021 or 2022 tax return, please complete Form T777S summarizing the home office expenses you incurred during the year.

The CRA has posted eligibility criteria under each method mentioned above to help determine who can claim this benefit.

If you would like our assistance in deciding which method is best for you, please do not hesitate to contact us!

The Upcoming 2021 Federal Budget & Potential Changes in Taxation

Leave a CommentThere have been significant changes to the Canadian economic landscape in the years since the 2019 Federal Budget was released. Most notably, the economic effects of the COVID-19 pandemic on the Canadian economy have been immense. The economic support programs introduced by the Federal government have been numerous and come with a significant cost.

Leading up to the 2021 Federal Budget, there has been speculation with regards to how the Federal government will, in effect, pay for the cost of the various economic support programs. Speculation has included changes to the capital gains inclusion rate, principal residence exemption, a wealth tax, and other measures.

The capital gains inclusion rate is the amount of capital gains that are considered taxable, and has been at 50% for the past 20 years. The taxable capital gain, being 50% of the capital gain, is taxed at a taxpayer’s marginal tax bracket according to their income level. For top earners in Ontario who are taxed at 53.53% on their incremental taxable income, capital gains are taxed at 26.765% (50% x 53.53%). There has been speculation that the 2021 Federal Budget will increase the capital gains inclusion rate to 75%. This would mean that an individual in the top marginal tax bracket in Ontario who would previously pay 26.675% on their capital gains would now pay 40.1475% (75% x 53.53%).

The principal residence exemption is, in brief, an exemption to the tax on capital gains which would otherwise result on the sale of an individual’s principal residence. In effect, the appreciation on an individual’s home is not taxed when the exemption is claimed. There is no maximum on this amount, although certain factors may prevent an individual from claiming the exemption. Speculation on changes to the principal residence exemption have included a limit to the exemption and a removal of the exemption.

A wealth tax is a complex and difficult endeavour for the Federal government to undertake. The concept of a wealth tax is not new, but then again, the definitions and legislation will require careful planning to avoid unintended consequences. Probate, an estate and administration tax, taxes the transfer of wealth from one generation to another and varies significantly among the provinces and territories of Canada. Probate may be considered a kind of wealth tax and may be changed by the various provincial budgets or the introduction of a federal estate and administration tax in the upcoming budget.

There are many different ways in which the upcoming 2021 Federal Budget may change taxation in Canada, and while we cannot know for certain what the changes will be until they are announced on April 19th, certain planning opportunities may be available to mitigate these changes.

If you would like our assistance in exploring potential planning opportunities for your specific tax situation, be sure to contact us.

Update: Work Space in the Home Expenses

Leave a CommentOn December 15, 2020, CRA published additional guidance with respect to claims for work space in the home expenses on the upcoming 2020 personal tax return. The guidance outlines details relating to the new temporary flat rate method, new optional detailed method, changes to the claims process, and new eligible expenses.

Temporary Flat Rate Method

The temporary flat rate method allows eligible individuals to claim a simplified expense of $2 per work day (up to $400) on their 2020 personal tax return. Work days include days that you worked full-time or part-time hours from home either due the requirement of your employer or voluntarily if your employer gave the option to work from home due to the pandemic. You must have worked from home more than 50% of the time for at least 4 consecutive weeks during the pandemic to be eligible.

You do not need to calculate the size of your workspace, keep supporting documents, or obtain a signed Form T2200S or Form T2200, from your employer to use this method.

The temporary flat rate method is not available if claims are being made for other employment expenses, such as vehicle expenses, or if your employer reimbursed all of your home office expenses. If your employer reimbursed some but not all home office expenses, you are still eligible to use this method.

Optional Detailed Method

The optional detailed method for home office expenses allows you to claim expenses you paid for the period you worked from home. Eligibility for the detailed method is similar to the flat rate method with the additional requirements that you obtain a completed signed Form T2200S, or Form T2200, from your employer and the expenses claimed are used directly in your work during the period.

The CRA has created a simplified Form T2200S and Form T777S as well as a new web calculator. The CRA has also stated that they will accept electronic signatures on Form T2200S, or Form T2200, for the 2020 tax year only.

The CRA has also published a list of home office expenses for employees and guidance on how to determine your work space use.

If you are expecting to make a claim on your 2020 personal tax return using the detailed method, you should reach out to your employer to ensure you get a signed T2200S. In addition, all supporting invoices should be kept to support the claim under the detailed method. To make a claim on your 2020 tax return, please complete Form T777S summarizing the home office expenses you incurred during the year.

If you would like our assistance in deciding which method is best for you please do not hesitate to contact us!